Are property taxes a silver lining to the slide in house values?

Whether homeowners can expect a short-term reprieve is a less-than-simple question

![]() By James R. Follain, Ph.D., and Barbara A. Follain, Cyberhomes Contributors

By James R. Follain, Ph.D., and Barbara A. Follain, Cyberhomes Contributors

Published: January 14, 2009

The news about housing prices continues to be bleak. By each of the main indexes, home prices dropped by more in the past 12 months than ever seen in a one-year period. For example, the National Association of Realtors reported in November that the average sales price of existing homes declined by more than 11 percent in the past year. Of course,declines in some parts of the country are even more severe.

We have been searching for any sliver of a potential silver lining amid these declines. One that might apply to you is a reduction in your property taxes. Here is our logic: Residential property taxes are typically based upon the value of your home, so if the value of your home declines, then your property taxes may also be expected to decline. We decided to investigate whether this simple argument bears some truth and, if not, why not.

This article is about our search for answers. As with so many other issues in today’s economy, the answers are not so simple, and there are numerous exceptions to the rule as we stated it.

The state of property taxes in the United States

In 2008, the U.S. Census produced one of the most comprehensive views of property taxes ever compiled. Of particular interest were the measurement of property taxes paid on residential properties for almost 800 counties and the ability to compare these taxes to property values and local incomes. Typically, measures of property taxes such as this do not distinguish between the property taxes paid by residential property owners and business owners. The data, from 2007, are readily accessible and nicely summarized by The Tax Foundation.

The average U.S. residential property tax bill in 2007 was $1,838. You can think about the tax burden as a percent of house value; the average property tax rate for owner-occupied properties was about 1 percent in 2007. Property taxes can also be expressed as a percent of the incomes of owner-occupied households, which averaged about 3.9 percent in 2007.

There is extraordinary variation around these averages. A nice graphic of the variation is available in a study by the National Association of Home Builders. This study also highlights one explanation for the variation: States vary widely in their reliance upon the property tax for their revenues. For example, New Hampshire does not tax wages and salaries but derives almost 43 percent of statewide government revenue from property taxes. New Jersey gets more than 35 percent from property taxes. On the other hand, Delaware, New Mexico and southern states such as Alabama, Arkansas and Louisiana obtain no more that 9 to 11 percent of statewide revenue from property taxes.

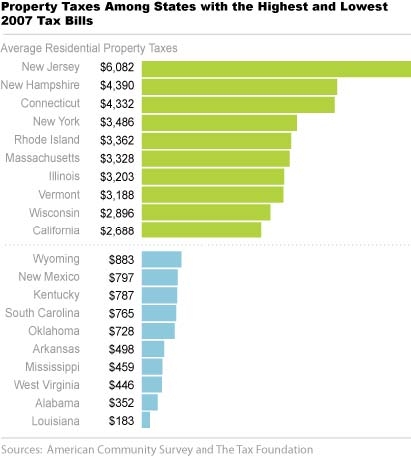

We capture the variation among states by reporting some of the outliers. Consider, for example, the variation among states in the dollar amount of taxes. Property tax bills for homeowners in New Jersey averaged $6,082 in 2007, the highest in the nation. Seven of the costliest 10 states are in the Northeast. Property taxes are much lower in some states, primarily in the South and West. At the bottom of the list is Louisiana, where property taxes are less than $200 per year.

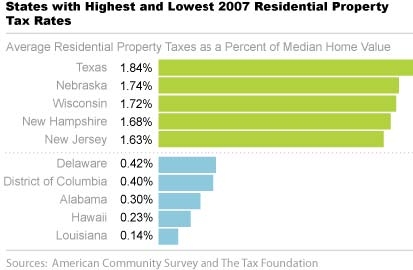

Another way of expressing property taxes is as a percent of property values. Arranging the 10 states with the highest and lowest property tax rates shows a somewhat different pattern. Louisiana is still at the bottom with a property tax rate of 0.14 percent, but Hawaii is also near the bottom. New Jersey is still among the top five, but Texas actually has the highest average property tax rate at 1.82 percent of median home value.

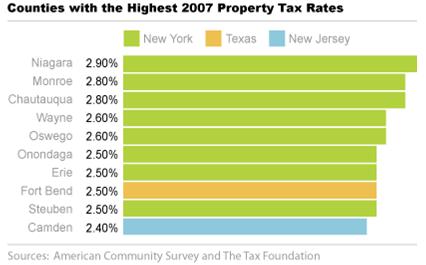

Drilling down to the local level, the 10 counties with the highest and lowest average tax bills are all in New York and New Jersey, which reflects a combination of relatively high property tax rates and high property values. New York’s Westchester County has the dubious honor of possessing the highest average property taxes among U.S. counties, at $8,422, with Hunterdon County of New Jersey just $200 behind.

We can do the same comparisons with property tax rates. Perhaps the most striking feature isthat eight of the 10 counties with the highest rates are also in New York state.However, these eight counties are in upstate New York, whereas Westchester andNassau are in downstate and near New York City. Property tax rates in theseareas are all in excess of 2.5 percent, or two and a half times the national average. The property tax rate in Niagara County is 2.9 percent of the median property value in the county. So, for example, the owner of the median-priced home in Niagara County, which is about $100,000, paid about $2,900 in property taxes in 2007.

We are keenly aware of the relatively high property tax rates in upstate New York. We lived in Onondaga County for many years while Jim was with Syracuse University. We lovedthe community and felt fortunate to raise our children in the area, but we remember being amazed that our property tax bill stayed about the same when we moved from Syracuse to Northern Virginia in 1998, even though the value of ourVirginia home was more than double the value of the home we sold in Syracuse.

Is there much connection between property tax levels and recent price declines?

Now we move to the heart of our inquiry. Are the areas with relatively high property taxes also those with the largest price declines? If so, perhaps

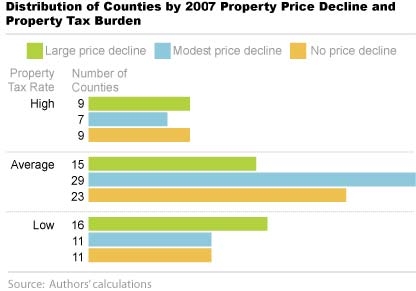

some relief is on the way. We did a wide variety of analyses using pricing data from Cyberhomes to identify a strong pattern — but found little. Counties with at least 500 sales in the second quarter of 2008 fall into threecategories of price declines (large, modest and none) and three property taxrate categories (high, middle and low). We find little connection. For example, only 7 percent of the 130 counties with at least 500 sales had property tax rates above 1.5 percent and experienced a price decline of at least 10 percent.The bulk of the counties are in the middle categories, which suggests one conclusion — many of the counties with relatively high property tax ratesare not those in which house price declines have been most dramatic.

Where are some ofthe places with relatively high property taxes that experienced substantialprice declines? There are many ways of defining this group. We focused oncounties with property tax rates in excess of 1.5 percent (median rate) andproperty taxes of more than $4,000 in 2007,and that experienced a price decline of at least 10 percent since 2007. Six counties met these criteria.

HillsboroughCounty, N.H., is at the top of the list. When you look at recent house price trends for Hillsborough County onCyberhomes, you can see that prices declined from an average of about $270,000 in July 2007 to about $230,000 in September 2008 (see Median EstimatedHouse Values chart). Since then property values have spiked up a bit, but theystill remain well below their peak values.

Four of the other six countiesare in New Jersey, which is another state with relatively large reliance uponproperty taxes for its revenues. For example, Camden County, N.J., southeast of Philadelphia, hasexperienced a price decline of more than 10 percent since mid-2007. Median property taxes in this county exceeded $5,300 in 2007, which was about 2.4 percent of median property values. Clearly, folks in this county may be hopeful of some property tax relief.

To provide a sense of the range of possible outcomes a property owner might expect, we compute two additional numbers foreach county. The first measures what would happen to the amount of property taxes if the property tax rate remains unchanged; in this case, property taxes decline exactly in proportion to the decline in house prices. The second measures the opposite extreme. It measures the property tax rate necessary to maintain the same amount of property taxes after the price decline. The twocolumns on the right side of the table above give an idea of the range of potential outcomes. For example, the property tax rate would have to increasefrom 1.68 percent to more than 2.4 percent in Hillsborough County to keepproperty taxes unchanged. Similarly, the property tax rate would have toincrease from 2.38 percent to 2.72 percent in Camden County to keep property taxrevenues unchanged.

What does history suggest might happen?

We’re not the only ones asking how property taxes might change in response to the declines in house prices. Economist Byron Lutz of the Federal Reserve Board recently published an exhaustive study, “The Connection between House Price Appreciation andProperty Tax Revenues.” He studied property tax revenues in all parts of theUnited States for the past 30 years or so. He is particularly interested in what happens to property taxes when house prices rise. Lutz finds that property taxes rise by about 40 percent of the rise in house prices, though the 40 percent hike in property taxes usually takes place gradually over the three or four years following the price hike. If this rule of thumb holds for Hillsborough County, homeowners might expect a decline in property taxes of about 12 percent — 40 percent of the decline in average prices — over the next few years.

Lutz also finds wide variation around this average. If the increase in house prices is relatively large, the rise in property taxes tends to be a little less than 40 percent. If house prices rise by a modest amount, then homeowners can expect more than a 40 percent rise in property taxes. Lutz also points out that there is very little data relevant to the particular question we are focusing upon: what happens following a period of declining house prices. The reason is that such a pattern has not been the dominant pattern in the United States for the past 30 years. In brief, we are in uncharted territory, so the 40 percent rule may not be a good one to rely upon in your community.

What we suspect will be new this time around

There are a couple of potentially critical factors at play that may affect the applicability of these historical patterns to the current environment. First and probably most importantly, county governments will have fewer safety valves to help lower property taxes during the current environment. For example, a local government often looks to its state government for additional revenues to make up for shortfalls in its property tax collections. In the current economic environment, though, many state governments are also under serious fiscal stress and will simply be less able to help. New York and New Jersey are prime examples, since both are being hit hard by the problems on Wall Street.

A second possibility involves the revolution in the availability of information about the value of one’s home. We have in mind the wealth of information that can be obtained at websites like Cyberhomes to educate homeowners about the values of their homes and those in their neighborhoods. Equipped with such information, we suspect that challenges to property assessments will be more common and better documented, especially in those areas experiencing substantial price declines.

Given such limited opportunities for state assistance, and an informed citizenry, expenditures on public education for kindergarten through 12th grade may well be at the center of upcoming demand for lower property taxes. We say this because K-12 public education is the major use of property taxes in most places. As a consequence, some difficult decisions will have to be made about whether to increase property tax rates or to cut back on spending for public education. Public school administrators, for example, will probably be asked to prioritize itseducational expenditures and to postpone or reduce some items less critical to the core education mission.

It is also important to understand that enthusiasm for property tax increases to support public education during these times of declining house prices may be weak among some groups. We particularly have in mind those folks at or nearing retirement and whose retirement savings may have also been particularly hard hit by the decline in the stock market of the past 18 months. In fact, another recent study by Economist Hui Shan of the Federal Reserve Board quantifies one potential effect of rising property taxes:increased mobility rates among the elderly. She estimates that an increase in annual property taxes can generate a substantially higher mobility rate among this group. As such, local and state government officials may be wise to consider tools such as circuit-breakers to ward off this effect.

In sum, we are not optimistic about property taxes serving as a silver lining for several reasons. First, although there may be some places where relief may be both deserving and possible,most of the places hit hardest by the declines in house prices — California, Nevada, Arizona and Florida — do not rank among the places with the highest property tax burdens. Second,even among those places where a property tax cut may be well-deserved, many local governments may be hard pressed to grant such relief because they are also experiencing financial stress in today’s environment. We encourage all involved to keep in mind the importance of public education,consider ways of postponing non-critical expenditures, and minimizing the potential impact of property tax increases upon the portions of the elderly community particularly hard hit by the double whammy of declines in the values of their homes and their retirement savings.

News & Insights

-

Green Light for GSA’s OASIS SB Vehicle

-

GAO Ruling Validates FI Consulting’s Financial Analysis